Market Insight – February 2024

Recent commentary by US Federal Reserve officials indicates that the FOMC is likely to ease policy in the coming months. As we are writing this in mid-February, US interest rate futures markets are pricing in between three- and four- 25bp eases before year-end, with a high likelihood of more following in 2025.

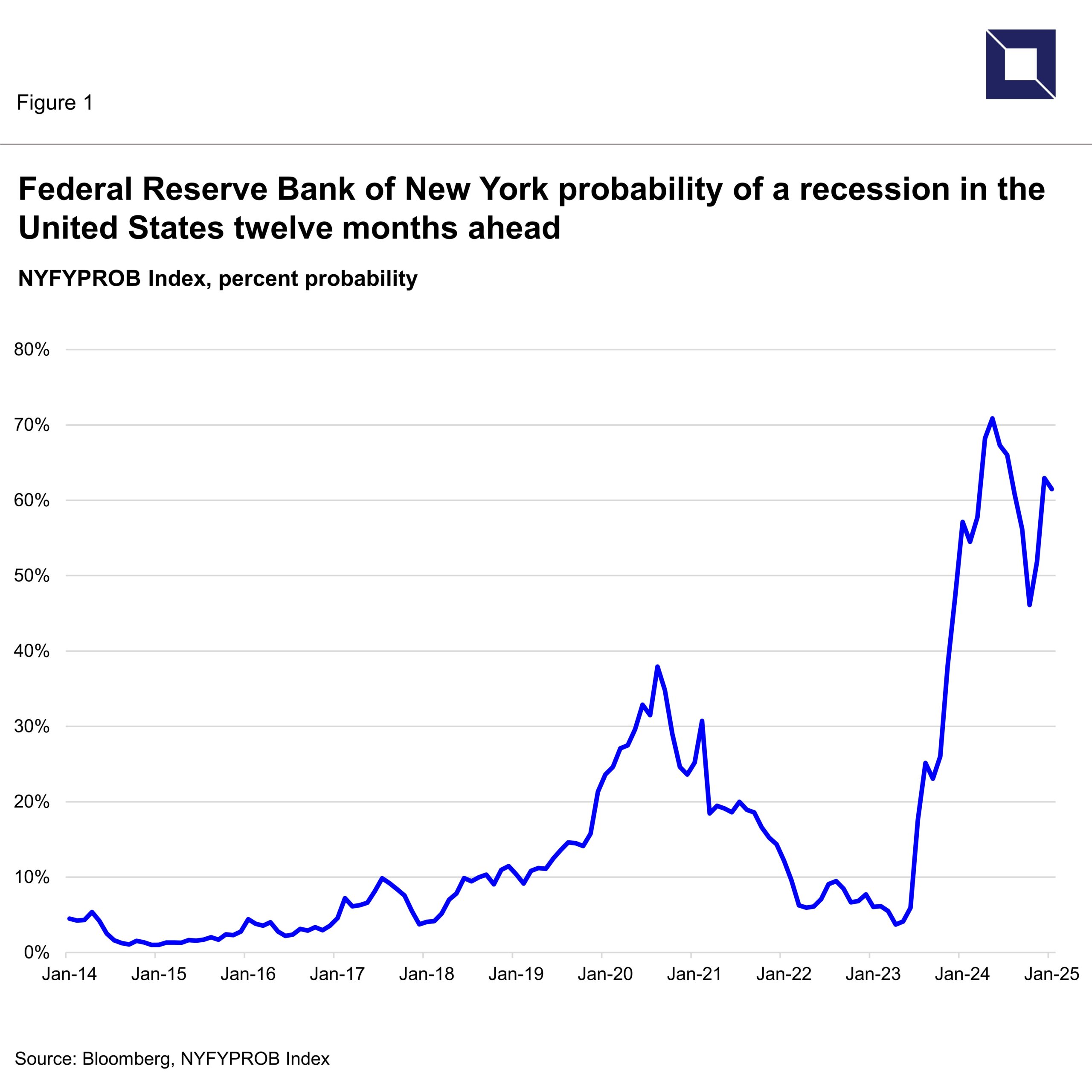

In January, a Federal Reserve Bank of New York (FRBNY) recession risk model based on the US Treasury yield curve implied a 61% chance of a recession beginning by January 2025 (Figure 1) (Estrella & Trubin, 2006). Given the signals from the Treasury market, and FOMC’s apparent easing bias, one might reasonably expect fixed income investors to be showing some anxiety about tightness in current financial conditions. But for now, this is not the case.

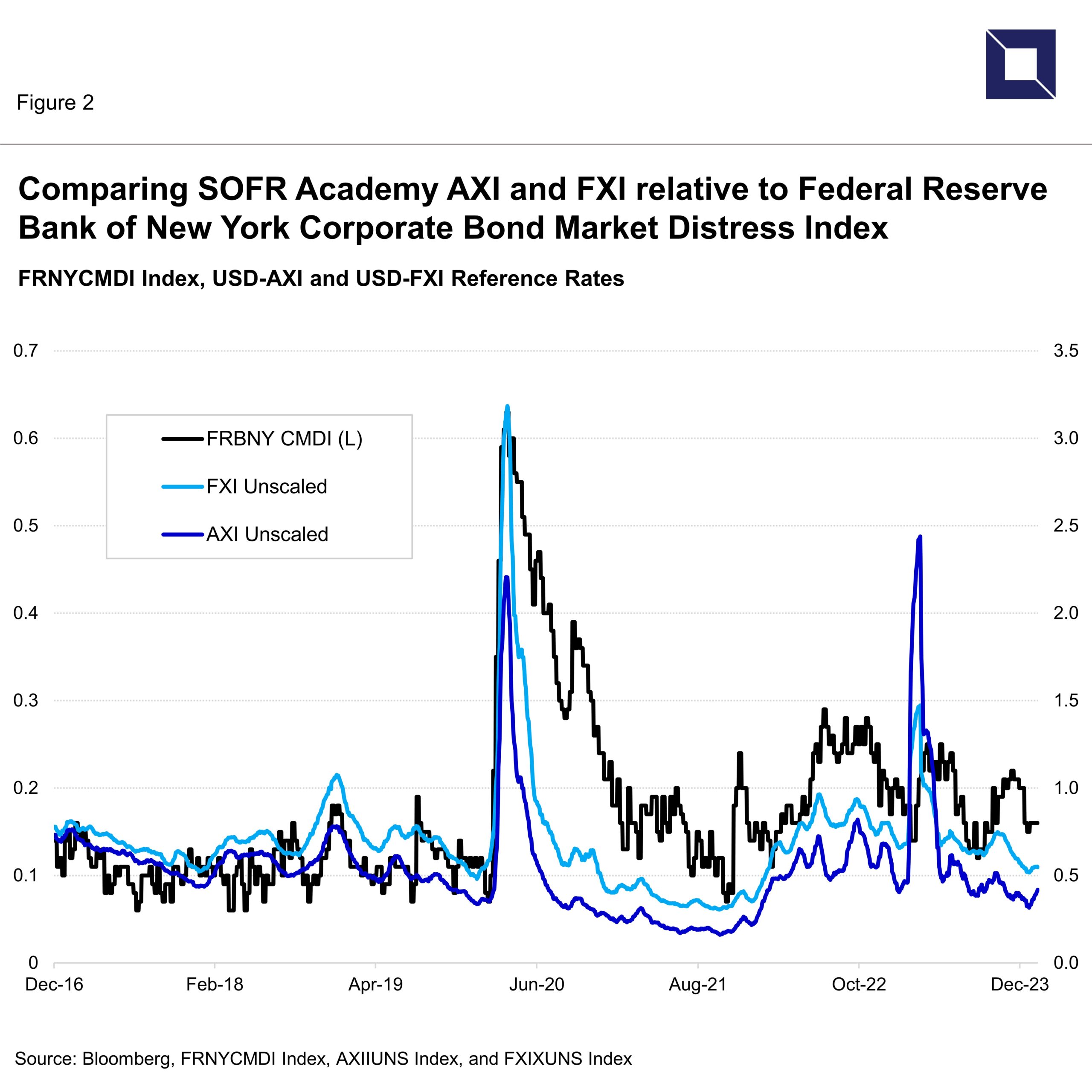

A view of financial market conditions is available from the FRBNY’s Corporate Bond Market Distress Index (CMDI) shows that there’s not much distress currently reflected in the US corporate bond market (Boyarchenko, Crump, Kovner & Shachar, 2021). The CMDI combines both primary market and secondary market measures and includes data on bond issuance volumes and primary market pricing as well as issuer characteristics. For the secondary market, FRBNY uses trading data available through the Financial Industry and Regulatory Authority’s Trade Reporting and Compliance Engine (TRACE) and includes measures that reflect both the central tendencies, and other aspects of the distributions, of volume, liquidity, nontraded bonds, spreads, and default-adjusted spreads.

SOFR Academy’s AXI and FXI indices have behaved similarly to FRBNY’s CMDI over the past several years (Figure 2). This should not be surprising given that CDMI, AXI and FXI have similar financial DNA – they each rely on corporate bond market pricing as a primary input and interpret significant changes in pricing as reflecting changes in credit market and economic conditions. But as Figure 2 shows, the performance of the three metrics has differed at times and it’s helpful for users of these metrics to understand why.

“Given the signals from the Treasury market, and FOMC’s apparent easing bias, one might reasonably expect fixed income investors to be showing some anxiety about tightness in current financial conditions. But for now, this is not the case.”– Alex Roever, CFA, Senior Advisor, SOFR Academy

Figure 2 demonstrates two episodes where the performance of the indices diverged. The first of these was in early 2020 around the onset of the pandemic when all three indexes spiked higher as markets reacted negatively to the initial news. While AXI rebounded relatively quickly in response to intervention by the Federal Reserve, FXI and CDMI recovered more slowly as it took time for fiscal and monetary support programs targeting non-banks to be crafted and implemented. The second notable episode occurred in March 2023 triggered by the failure of two large regional banks. AXI levels spiked more than the others (given the high concentration of bank debt in the AXI), but then recovered following the resolution of these failures.

In contrast to CDMI, AXI and FXI have been developed to serve as usable benchmarks for bank lending and related derivatives risk management applications. Both AXI and FXI index are weighted averages of credit spreads for unsecured debt instruments with maturities ranging from overnight to five years, with weights that reflect both transactions volumes and issuance volumes. The primary difference is that AXI focuses on bank-related funding in the in the bond and money markets, while FXI builds on the AXI chassis and adds non-bank corporate credit transactions. The average credit spreads represented by AXI and FXI can then be combined with SOFR as a market-based measure of average funding costs for bank and non-bank issuers.

Consequently, because of the way they are constructed, AXI and FXI can function as the credit component of credit sensitive interest rate benchmark, and as indicators of evolving financial conditions (Berndt, Duffie & Zhu, 2023).

Alex Roever, CFA, is a Senior Advisor at SOFR Academy ([email protected]).

This note is provided for informational purposes by SOFR Academy, Inc. (SOFR Academy), an economic education and market information provider. This note is not designed to be taken as advice or a recommendation for any investment decision or strategy. Readers should make an independent assessment of relevant economic, legal, regulatory, tax, credit, and accounting considerations and determine, together with their own professionals and advisers, if the use of any index is appropriate to their goals. Neither the Invesco / SOFR Academy USD Across-the-Curve Credit Spread Index (AXI), nor the Invesco / SOFR Academy USD Financial Conditions Credit Spread Index (FXI) are associated with or sponsored by the Federal Reserve Bank of New York or any regulatory authority. Additional information about SOFR Academy, AXI and FXI can be found here.

Copyright 2024 SOFR Academy, Inc. All rights reserved