Robustly defined credit spreads that can be used in conjunction with SOFR to form a credit sensitive interest rate in loans and derivatives.

Transformational Change. Transforming Leaders.

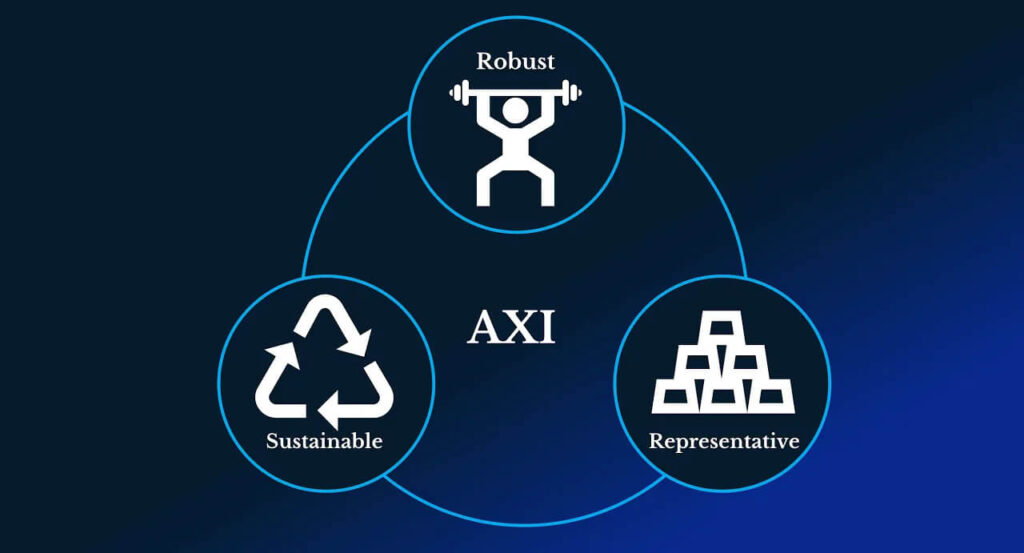

The benchmark spreads are computed from a sufficiently large pool of market transactions so that it can underlie commercial lending applications as well as actively traded derivatives instruments used by banks and their borrowing customers to hedge their floating-rate exposures, without significant risk of statistical corruption or manipulation. Expert judgement is not used nor are executable quotes. Adopting an across-the-curve methodology ensures that the maximum number of transactions are captured within the index. USD-AXI is not limited to the short-term unsecured markets that once underpinned LIBOR. USD-FXI is even more robust.

Since the 2008 Global Financial Crisis, banks no longer fund themselves at LIBOR and have shifted their funding further out the yield curve. USD-AXI is highly correlated with banks’ funding costs because it captures this deeper pool of funding transactions. The index is a weighted average of credit spreads for U.S. bank unsecured debt instruments with maturities ranging from overnight to five years, using weights that reflect both transactions volumes and issuance volumes. The input data is obtained only from publicly available sources.

USD-AXI and USD-FXI reference rates were designed to maintain their hedge effectiveness and robustness over time and can be reliably computed in all economic conditions, including in times of market stress. The indices automatically adapt to future changes in bank funding composition ensuring their representativeness and robustness are sustained through time. The spreads work in conjunction with SOFR. If a loan references USD-AXI or USD-FXI, it will also reference SOFR, so the development of a USD-AXI and or USD-FXI market does not imply less usage of SOFR, and the credit spreads can develop without diverting any liquidity from SOFR (Tuckman, 2023).

Detailed methodology documentation is available and underlying statistical metrics are published by the AXI & FXI authorized benchmark administrator each business day. Index history is available from 2016 and links have been published so that market participants can obtain samples of input files. Consistent with the direction contained within the FSOC’s 2023 Annual Report, market participants have sufficient information to perform an evaluation of USD-AXI and or USD-FXI prior to referencing these spreads in financial instruments.

Independent research shows that under a SOFR-only regime, in times of market stress, it is likely that bank credit lines will be maxed out, creating a potential threat to financial stability. Heavy simultaneous drawdowns by borrowers may deplete bank capital, reducing capacity for new term loan origination and drying up liquidity in financial markets. The absence of a credit-sensitive element in the reference rate removes the disincentive for borrowers to draw down (Marshall, et al, 2019).

A lender may offer better terms on revolving lines of credit by linking the drawn rate on its lines to the sum of SOFR and USD-AXI (or USD-FXI). Doing so lowers the expected net cost to the bank should its lines be heavily tapped in some future market stress event when wholesale bank funding spreads are elevated. It also lowers the overall (average) expected cost of funds for the borrower (Cooperman, Duffie, Luck, Wang & Yang, 2023).

The existence of benchmarks have been shown to improve market transparency, lowering the informational asymmetry between dealers and their customers regarding the true cost to dealers of providing the underlying asset. This suggested a possible public-welfare role for regulators regarding which markets should have a benchmark, and also in support of the robustness of benchmarks to manipulation (Duffie, Dworczak & Zhu, 2014).

In IBM Promontory‘s opinion, AXI and FXI fully implemented Principle 6 of IOSCO’s Principles for Financial Benchmarks. AXI is designed to measure the aggregate recent average cost of wholesale unsecured debt funding for U.S. bank holding companies and their U.S. banking subsidiaries. The unscaled AXI credit spread is then calculated as a weighted average of the transaction notional volumes and maturities of such instruments. IBM Promontory’s case study is available here and their full report is available here.

AXI and FXI fully implemented Principle 7 of IOSCO’s Principles for Financial Benchmarks. AXI and FXI short-term and long-term spreads are fully based on observable, bona fide, arms-length transactions. Indicative bids/offers, executable bids/offers or estimates of any type are not used in constructing AXI/FXI spreads. IBM Promontory’s case study is available here and their full report is available here.

Based on the limited assurance review performed previously, and Promontory’s conclusion that SOFR

Academy and the Administrator appear to have reasonably addressed the recommendations in the Report,

IOSCO Principles 6, 7, and 9 appear to be fully implemented for AXI and FXI. IBM Promontory’s case study is available here and their full report is available here.

No. AXI is a spread which is added to SOFR. AXI is not a proxy for any interest rate. AXI can be used in conjunction with overnight SOFR (published by the NY Fed), CME Term SOFR, or other SOFR variants to form a credit-sensitive interest rate benchmark for loans, derivatives, and other products.

Yes. In 2024, IBM Promontory performed a review of certain IOSCO Principles for Financial Benchmarks concluding that Principles 6, 7, and 9 are fully implemented for USD-AXI and USD-FXI. IBM Promontory’s case study is available here and their full report is available here.

No. Whenever a loan is indexed to a AXI, it would also reference SOFR. So, use of a credit spread index does not imply less frequent reference to SOFR.

Please submit your question through the contact form at the bottom of this website.

SOFR Academy engaged with IBM Promontory to conduct an in-depth evaluation of the AXI and FXI adherence to the IOSCO principles.

“Specifically, borrowers may find the availability of low cost credit in the form of SOFR-linked credit lines committed prior to the market stress very attractive and borrowers may draw-down those lines to ‘hoard’ liquidity. The natural consequence of these forces will either be a reduction in the willingness of lenders to provide credit in a SOFR-only environment, particularly during periods of economic stress, and/or an increase in credit pricing through the cycle. In a SOFR-only environment, lenders may reduce lending even in a stable economic environment, because of the inherent uncertainty regarding how to appropriately price lines of credit committed in stable times that might be drawn during times of economic stress,” (Marshall, 2019).

“We believe a sensible and practical way to address these risks is to create a SOFR-based lending framework that includes a credit risk premium. That framework could consist of a dynamic spread that reflects changes in banks’ cost of funds over forward-looking term periods and is added on a periodic basis to SOFR-based rates. With more closely aligned borrowing and lending rates, banks will be more willing and able to extend credit during both good times and bad” (Marshall, 2019).

Recent research uses data from the Federal Reserve’s FR2052a report and Y14Q data collection to show that the inclusion of a credit sensitive element in the base rate of revolving lines of credit, which is the primary form of lending in the U.S., supports the provision of credit by banks and therefore financial stability, whilst also lowering the expected average cost of financing for American borrowers (Cooperman, Duffie, Luck, Wang, & Yang, 2024).

To enhance the efficiency, transparency, and stability of financial markets.

We are committed to honesty, transparency, and ethical behavior.

We design, build, and deploy enduring products grounded in robust academic research that promote access to credit which supports economic activity.

We strive to be at the forefront of financial innovation, continuously seeking new ways to improve our products.

Benchmark due diligence

Thought Leadership

Systems and operations

Client Communications

SME Support

Risk Identification

Training

Contract Management

Please fill out the form to enquire and a member of our team will be notified.

Please note: while we appreciate your questions, we are unable to respond to all inquiries. Required fields are marked with an asterisk (*).