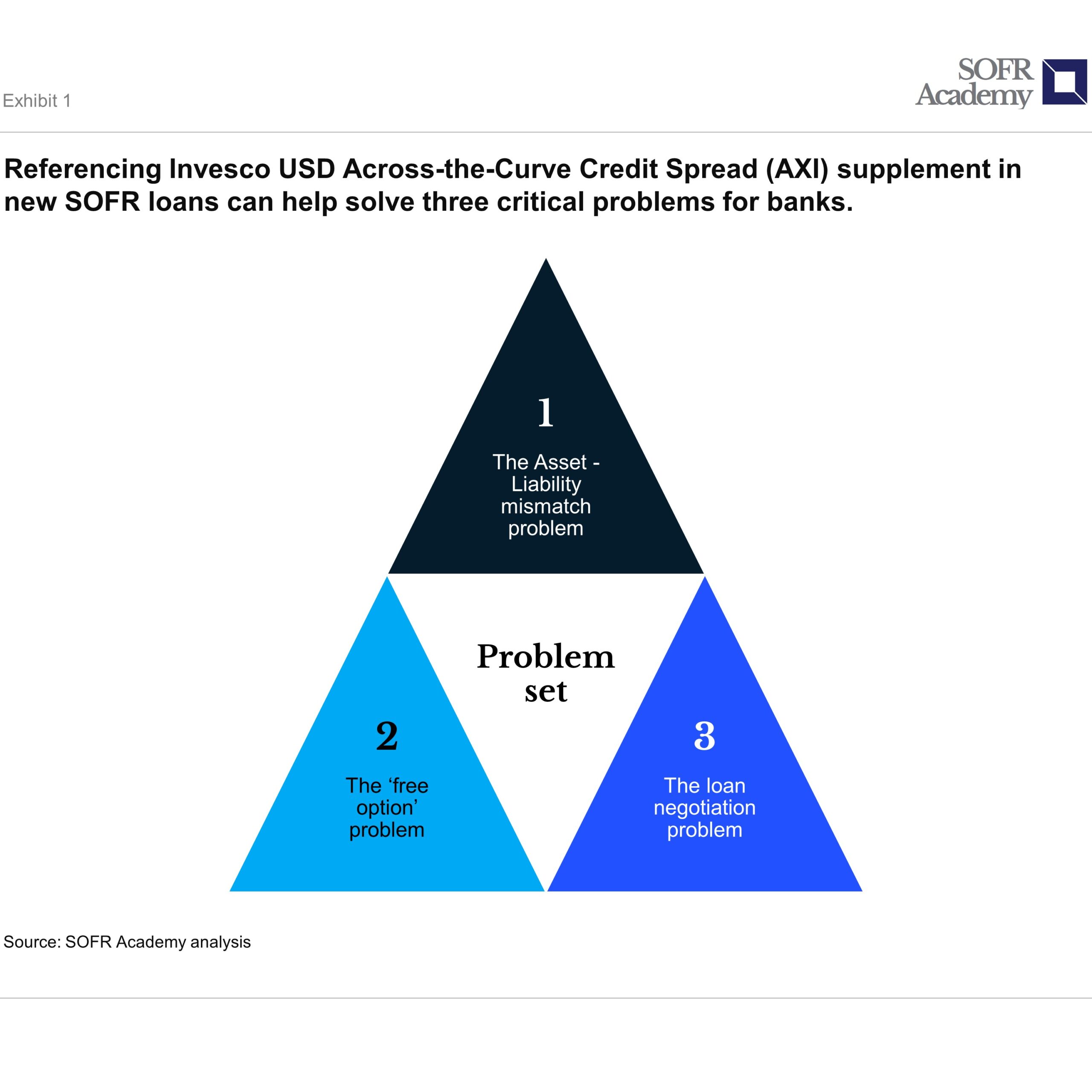

The provision of credit across the United States economy, including in bad times, enables firms to weather disruptions in their business that may impair their cash flow and limit their ability to meet commitments to suppliers and employees. American banks play an important role as liquidity providers. The transition away from the once ubiquitous and now broken LIBOR benchmark towards new robust risk-free-rates such as SOFR has created fresh challenges for bank lenders because the two benchmarks are economically different. We discuss three of these challenges and explore how referencing Invesco’s USD Across-the-Curve Credit Spread Index (AXI) supplement in new SOFR-based loans can help solve them.

After the Great Financial Crisis banks tended to fund themselves further out the yield curve because of new Basel rules. In todays financial system, “very few people borrow at the short end”, according to Federal Reserve Chairman Jerome H. Powell. This trend has left the once most heavily referenced interest rate benchmark, LIBOR, with an insufficient number of underlying transactions rendering it unfeasible. Recent academics studies, including in China (Li, Zhang, Zhang, Zhang, 2022), indicate that this trend of banks’ increasing reliance on longer term funding is not limited to the United States.

“Very few people borrow at the short end”– Federal Reserve Chairman Jerome H. Powell, November 2, 2022

The transition away from LIBOR to more robust rates such as SOFR has significant implications, including because they are fundamentally different benchmarks that can move in opposite directions in times of market stress, which presents important risks for banks. The continued provision and availability of credit across the United States is critical from the perspective of lenders, borrowers and policymakers. Leading banks will take a longer term view and consider the risks and opportunities in connection with their balance sheet in good economic times, and in bad.

1. The Asset – Liability mismatch problem

It is common in the United States for bank lenders to pre-agree revolving lines of credit with American corporate borrowers. The Wall Street Journal recently reported (Broughton & Trentmann, 2022) that some CFOs are boosting their credit lines now as insurance against a potential recession. Data from the onset of the pandemic indicates that companies tend to draw down on these revolving credit facilities to add cash to their balance sheets during an economic shock or periods of financial distress.

Whilst the onset of the pandemic was unanticipated and drawdowns were largely reactive in nature, much has been discussed about the potential for the economy to slide into a recession in 2023 and CFO’s at companies such as restaurant chain franchise Dine Brands Global Inc. (NYSE: DIN), utility company Xcel Energy Inc. (NASDAQ: XEL), and Bombardier Inc. (OTCMKTS: BDRBF) are currently increasing credit lines proactively – this can create three critical problem for banks.

In the past, credit facilities referenced short term credit sensitive rates (which are no longer feasible), these rates tend to jolt higher in periods of market stress and provide a disincentive for companies to borrow as rates move higher. That disincentive no longer exists in a SOFR-only environment because SOFR is a risk-free rate and tends to move lower in an economic crisis. This potential asset – liability mismatch between the rates at which banks lend and borrow was anticipated by a group of banks that wrote to bank regulators in September 2019: “During times of economic stress … the return on banks’ SOFR-linked loans would decline, while banks’ unhedged cost of funds would increase, thus creating significant mismatch between bank assets (loans) and liabilities (borrowings).”

New research by leading academics at the Federal Reserve Bank of New York and the Stanford Graduate School of Business confirm this asset – liability mismatch problem (Cooperman, Duffie, Luck, Wang, and Yang, 2022). The academic authors use high granularity balance-sheet data collected in the FR2052a dataset—collected to monitor the liquidity profile of large US BHCs— allowing them to pin down bank funding risk for large US Bank Holding Companies in much more detail than was possible in prior work.

Market participants have demonstrated a strong preference to reference SOFR in new transactions which now receives the vast majority of market liquidity, including in the lending markets. Referencing a credit spread supplement to SOFR such as Invesco’s USD-AXI in new credit facilities, which is highly correlated with bank funding costs, can provide greater balance sheet control for bank lenders because it allows them to avoid the potential asset liability mismatches that they are worried about.

Like to view the latest Invesco AXI rates?

Visit the Invesco / SOFR Academy AXI website >

To account for the economic differences between LIBOR and SOFR, a five-year historical median of the difference was frozen on March 5, 2021 after industry consultation. These spreads are 11.448 bps for hardwired 1M USD LIBOR contracts falling back to 1M SOFR and 26.161 bps for hardwired 3M USD LIBOR contracts falling back to 3M SOFR. When used in legacy loans, as we have communicated, some concern exists that if the historical fixed spreads differ to market-based credit spreads at the time of LIBOR cessation, this could result in market frictions with significant and avoidable value transfer. Measures of market credit conditions have been fluctuating, sometimes rapidly (see Exhibit 2), and applying a fixed credit spread based off of a historical relationship can prove problematic.

2. The ‘free option’ problem

Agreeing pre-committed credit lines linked only to SOFR, which can be drawn at any time, gives the borrower a ‘free option’ to draw down at potentially lower rates during times of economic stress. Pre-committed revolving credit lines tend to be drawn heavily when bank funding markets are stressed, presenting an important funding risk to banks (Cooperman, et al, 2022). The aforementioned letter from a group of banks who wrote to bank regulators in September 2019 goes on to say that: “Specifically, borrowers may find the availability of low cost credit in the form of SOFR-linked credit lines committed prior to the market stress very attractive and borrowers may draw-down those lines to ‘hoard’ liquidity.”

“…longer-term changes—such as those associated with labor supply, deglobalization, and climate change—could reduce the elasticity of supply and increase inflation volatility into the future”– Federal Reserve Vice Chair Lael Brainard, November 28, 2022

The concern is that significant bank funding risk can be created by this phenomenon, a risk that previously did not exist in a LIBOR-based world and may not be fully understood or quantified by bank balance sheet managers. Moreover, this risk may be difficult to hedge and the cost of credit-line draws may not be able to be passed on, forcing the bank to obtain new funding at the same time as the market is experiencing economic stress, potentially exacerbating funding conditions in a self-reinforcing nature which could have financial stability implications.

In terms of the quantum of exposure, Cooperman, et al (2022), found that at the end of 2019, the largest 20 banks alone had around $1.3 trillion of undrawn credit line commitments. Referencing a robustly defined credit spread such as USD-AXI in pre-committed SOFR-linked credit facilities can help solve this ‘free option’ problem because the interest rate on the loan will move higher in times of market stress providing a disincentive for borrowers to draw down at those times. And if they do, the bank is compensated commensurate with their contemporaneous cost of funds.

3. The loan negotiation problem

Loan negotiations between lender and borrowers have become more complicated in a SOFR-only environment, exacerbated by an uncertain macroeconomic backdrop and a once in a generation interest rate tightening cycle. Inflation around the globe is higher than desired by many central banks and “longer-term changes—such as those associated with labor supply, deglobalization, and climate change—could reduce the elasticity of supply and increase inflation volatility into the future,” according to Federal Reserve Vice Chair Lael Brainard.

This uncertainty across interest rates and funding is making loans more difficult to negotiate and price. Adding to this challenge and in connection with banks’ funding uncertainty, as we have shown, there continues to be a lack of consensus on new SOFR-linked loan pricing regarding the treatment of the credit spread adjustment.

“Borrowers don’t want to pay the 26 basis point fixed credit spread”– LIBOR transition lead at American industry association

Turning to the remediation of legacy cash products, one of the primary reasons that borrowers are hesitating to transition loans to SOFR is because the fixed credit spreads, which are calculated off of five years of history, are higher than contemporaneous market based spreads. Put simply, “borrowers don’t want to pay the 26 basis point fixed credit spread”, according to one LIBOR transition lead at a large American industry association, referring to the 3-month tenor. Further bank lenders do not want to take on the conduct risk of ushering a borrower into a outcome that is economically disadvantageous for them. Referencing an independently calculated and unquestionably representative credit spread supplement such as Invesco USD-AXI, that is calculated in a regulated environment, can improve the efficiency and fairness of loan negotiations.

ABOUT THE AUTHOR

Marcus Burnett is chief executive of SOFR Academy, based in New York.

DISCLAIMER

SOFR Academy supports SOFR, and near risk-free rates. Over time, we also support robustly defined credit spread supplements such as AXI and FXI which can be used in conjunction with risk-free rates. The article does not set out economic or credit conditions forecasts and should not be treated as doing so. It also does not provide legal analysis, including but not limited to legal advice. This note does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions. Invesco Indexing LLC is an indirect, wholly owned subsidiary of Invesco Ltd. The group is legally, technologically and physically separate from other business units of Invesco, including the various global investment centers. SOFR is published by the Federal Reserve Bank of New York (The New York Fed) and is used subject to The New York Fed Terms of Use for Select Rate Data. The New York Fed has no liability for your use of the data. AXI is not associated with, or endorsed or sponsored by, The New York Fed, or the Federal Reserve System. Darrell Duffie, The Adams Distinguished Professor of Management and Professor of Finance at Stanford Graduate School of Business, is a co-author of the proposal for AXI, but has no related compensation or other affiliation with its commercialization. Any prospective user of AXI or FXI that would intend to also use CME Term SOFR in developing an interest rate for Cash Market Financial Products or OTC Derivative Products would require a license with CME Group for use of CME Term SOFR.