Market participants in the United States have yet to coalesce around industry standard for pricing commercial loans in a post-LIBOR world. For bank lenders, adding an independently calculated and robustly defined credit sensitive spread to SOFR that is highly correlated with bank funding costs helps manage potential funding mismatches and reduces conduct risks. For borrowers, it enhances transparency and fairness. For policymakers, it reduces moral hazards and promotes financial inclusion.

In September 2019, a group of U.S. regional banking organizations wrote to U.S. regulators indicating their support for SOFR. They also expressed concern with using SOFR on a stand-alone basis in lending products, which could adversely affect credit availability. LIBOR and SOFR behave very differently in times of economic stress (Jermann, 2020). These regional banks, who play a vital role in the extension of credit across the U.S. domestic economy, suggested that an alternative framework could consist of a dynamic spread that reflects changes in banks’ cost of funds over forward-looking term periods and is added on a periodic basis to SOFR-based rates.

In response to this letter, former Vice Chair for Supervision Randal Quarles, former Comptroller of the Currency Joseph Otting, and former Federal Deposit Insurance Corporation Chair Jelena McWilliam shared a plan for “exploring such a supplement to SOFR”.

This led to the establishment of Credit Sensitivity Group Workshops (CSG) which were held throughout 2020 and chaired by Nate Wuerffel, Senior Vice President at the Federal Reserve Bank of New York. The CSG workshops were separate from and supportive of the work of the Alternative Reference Rates Committee (ARRC). It was at these sessions that Stanford University Professor Darrell Duffie and Australian National University Professor Antje Berndt introduced the concept of Across-the-Curve Credit Spread Indices (AXI) as an add-on to SOFR to both the Official and Private sectors. A volume weighted across-the-curve approach maximizes the number of underpinning transactions and also future-proofs the index because it automatically adapts to future changes in bank funding composition (Berndt, Duffie, Zhu, 2020). See Exhibit 1 for further details on desirable qualities of a credit sensitive index.

Regarding spread adjustments for new SOFR-based loans, there have been a number of different approaches suggested to date. One was to apply static spread adjustments: 10 basis point spread adjustment for one-month SOFR, 15 basis points for three-month SOFR, and 25 basis points for six-month SOFR. Another approach was to price with no spread adjustment at all to SOFR, but instead to incorporate the spread adjustment directly into a higher overall margin.

Banks who would like to settle on a uniform and optimal pricing structure for loans must consider several factors in addition to the economics. Market leading banks will value the long game over short term profits, placing clients and customers at the heart of the decision-making process, whilst also prioritizing the financial stability and efficiency of the broader market. We suggest six key considerations for banks in this decision process:

1. Prioritize safety and soundness

“Let’s reflect on how far we have come in what was always a challenging climb, but let’s also make sure we complete the job properly and safely descend the mountain that is Libor.”

― Andrew Bailey, Governor of the Bank of England

The core reason that the global market is shifting away from the use of Interbank Offered Rates is to uphold the safety and soundness of the financial system. There are no longer enough transactions with which to compute LIBOR and banks are now more likely to fund themselves further out the yield curve through wholesale transactions. This dearth of transactions left LIBOR subject to manipulation. In consultation with some of the brightest financial minds in the world, the ARRC spent nearly a decade in selecting SOFR as USD LIBOR’s preferred replacement.

Underpinned by approximately $1 trillion in daily transactions, SOFR can and should form the bedrock of the US-Dollar denominated financial system. For a bank to choose a base rate for a loan that does not reference SOFR invites heightened regulatory scrutiny and creates avoidable business uncertainty. It would also run counter to the directives of the Financial Stability Board (the body tasked with coordinating LIBOR transition at the international level), which has specifically recommended global usage of near risk-free rates. Furthermore, the vast majority of products currently referencing USD LIBOR will shift to SOFR, where market participants will find the deepest levels of liquidity and the greatest market efficiency.

2. Minimize conduct risks deliberately

“There is only one boss. The customer.”

― Sam Walton, founder of Walmart

Conduct risk is generally defined as the risk that clients or customers are treated unfairly. A theme that has emerged throughout LIBOR transition is the largely agreed upon outcome that borrowers and consumers should not be left worse off due to LIBOR transition. Banks face the specific challenge of deciding what constitutes a “fair” credit spread over SOFR to account for future changes in their cost of funding. Moreover, many banks simply do not want to price the credit spread themselves. The fact that the market has yet to coalesce around a unified approach (Coffey, 2021) is one of the reasons that the transition to SOFR has been slower in the US-dollar lending markets.

Leading banks will select a credit spread add-on to SOFR for new loan contracts that is not based on the judgment of market participants or traders, but on actual transactions, thereby minimizing conducts risks. Moreover, relying on “expert judgement” would mirror the core inadequacies of LIBOR itself. By referencing a robustly defined credit spread that is calculated and administered in a regulated environment by an independent third party, bank lenders reduce conduct risks. This also improve operational efficiencies for the bank because the burdens of governance, controls, documentation, and communication are lighter when the funding credit spread is determined independently by an arm’s length third party. Indeed, policymakers have clearly telegraphed that a SOFR-referenced loan carries a lower regulatory burden than a non-SOFR loan.

Utilizing an add-on to SOFR such as AXI reduces search costs for the borrower, can improve matching efficiency, and increases participation by less-informed agents. The least sophisticated investors will likely prefer their transactions to be executed at a standardized time via an index, encouraging them to participate in markets when incentives for good execution are supported by the existence of reliable benchmarks. These are some of the fundamental benefits of referencing an index versus negotiating bespoke agreements (Duffie & Stein, 2015).

The transaction-based funding credit spread selected by banks should obviously highly correlate with their cost of funds rather than historical LIBOR – after all, LIBOR is being discontinued because it was a flawed benchmark. A Financial Stability Report (FSB, 2014) found that “bank funding models have been evolving radically over the past decade – unsecured interbank market activity in many jurisdictions has declined noticeably as banks have increased their reliance on broader wholesale unsecured and secured financing – reference rate designs have not kept up with the developments in the wholesale funding market”.

“the percentage of U.S. bank funding directly tied to wholesale unsecured borrowing at terms similar to the most widely used LIBOR tenors might be 2-3 percent.”– David Bowman, Chiara Scotti, and Cindy M. Vojtech – U.S. Federal Reserve Board Economists

Indeed, Federal Reserve Board economists Bowman, Scotti, Vojtech, 2020 showed that “the percentage of U.S. bank funding directly tied to wholesale unsecured borrowing at terms similar to the most widely used LIBOR tenors might be 2-3 percent.” Therefore, with respect to large U.S. banks, it seems logical to conclude that there may be increased uncertainty as to whether an index or spread that is highly correlated with LIBOR seeks “to achieve, and result in an accurate and reliable representation of the economic realities of the interest it seeks to measure” which constitutes Principle 6 ‘Benchmark Design’ of the internationally agreed and recognized International Organization of Securities Commissions (IOSCO) Principles for Financial Benchmarks.

The implication is a greater threshold for banks when rationalizing the choice of a credit spread that correlates highly with LIBOR versus one more aligned with actual bank funding costs, such as AXI. Ideally, the credit spread would be calculated using input data from publicly available and regulated data sources to maximize transparency and promote index credibility.

3. Promote market transparency

“I think transparency is at the heart of efficient markets.”

― Gary Gensler, Chairman of the U.S. Securities and Exchange Commission

Referencing a credit-spread add-on to SOFR has an additional benefit of promoting transparency when borrowers delegate their decisions to agents, who may not always exercise optimal fiduciary responsibility for their clients. Consider this situation adapted from Duffie & Stein, 2015 to the lending market: Suppose a borrower is told by her broker, “We obtained an excellent base rate for your loan of 3-month CME Term SOFR plus a 15 basis points credit spread adjustment” (the borrower’s standard margin would then be added to this base rate, the same way it was added to LIBOR in the past). Absent a defined credit spread index, the borrower could not easily validate the brokers claim and may be suspicious of the potential for dishonest service. However, if there is a simultaneous published credit spread index fixing that correlates highly with bank funding costs by design, then the broker’s claim of good execution is easily verified. Reducing this moral hazard benefits the lender, the borrower, and the agent. U.S policy makers prioritize market transparency and financial inclusion.

A credit spread add-on to SOFR such as AXI also provides valuable pre-transaction price transparency, offering less informed market participants a better idea of the ‘going price’. By reducing the informational asymmetry of ‘buy-side’ market participants relative to dealers, indexes encourage greater market participation, lower the cost of delays associated with ‘shopping around’ and negotiating for a better price, and improve the ability of markets to efficiently match buyers with the most cost-effective sellers, and vice versa (Duffie, Dworczak, Zhu, 2014).

Would you like to download AXI sample data?

Visit our dedicated Invesco / SOFR Academy AXI microsite ›

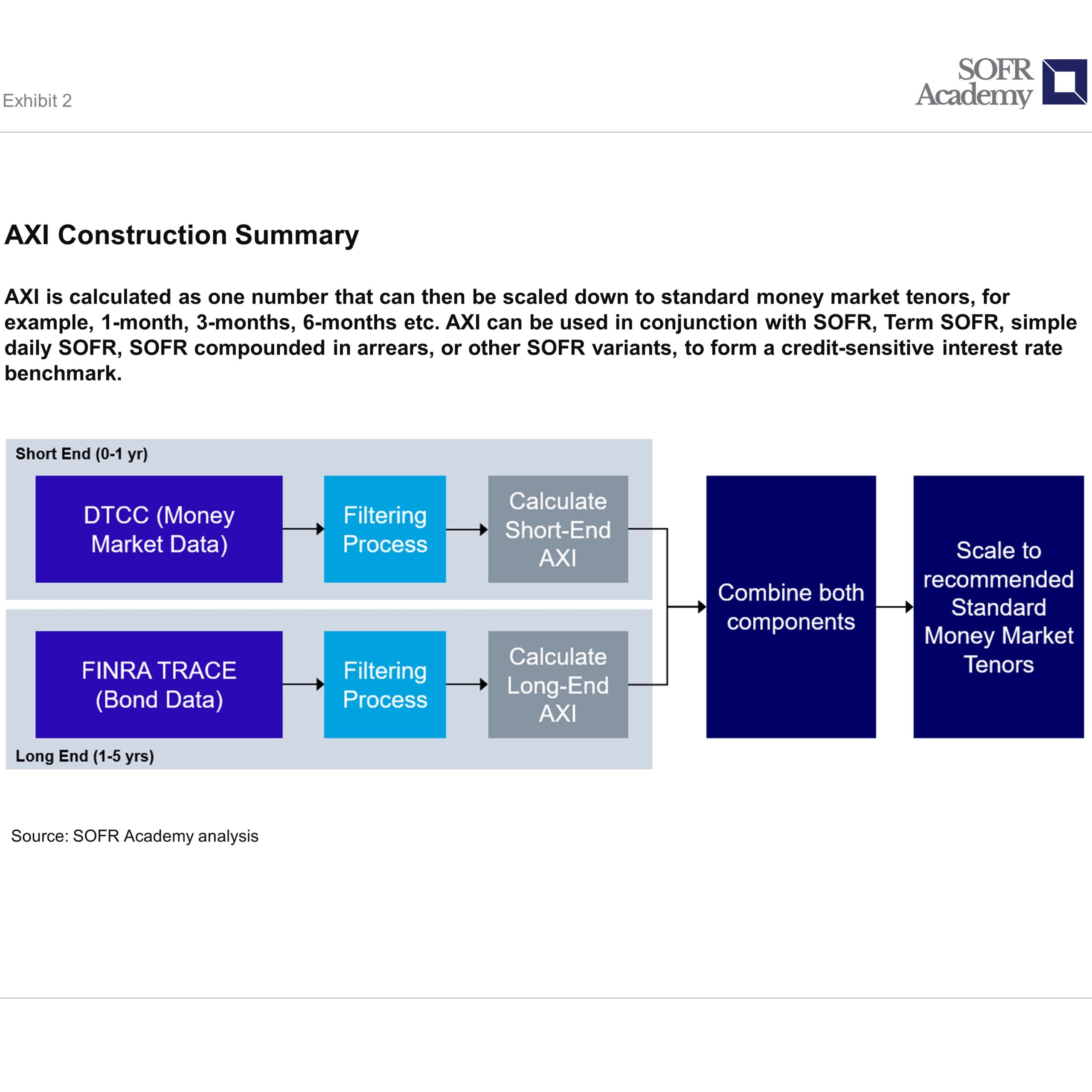

Transparency is even a key attribute of AXI’s construction methodology. AXI is comprised of two main components: the short end, and the long end. For SOFR Academy’s AXI prototype spreads (see Exhibit 3), the short end input file is published each business day by the Depository Trust & Clearing Corporation (DTCC) at approximately 5.30pm EST and the long end input data file is published by Financial Industry Regulatory Authority’s (FINRA) Trade Reporting and Compliance Engine (TRACE) at approximately 7.30pm EST. After the algorithm is computed, the index is published the following business day around 8am EST. Standardizing the execution and publication time of AXI also promotes the development of a hedging market to facilitate risk-transfer.

4. Respect the Borrower’s margin

“We will never forget that the most important thing we do is to run a healthy and vibrant company that is here to constantly serve our clients with responsible banking.”

― Jamie Dimon, CEO of JP Morgan

Banks have historically made loans to borrowers by assigning an idiosyncratic margin over LIBOR that is reflective of the creditworthiness of that borrower. Looking ahead, the question is whether a credit spread adjustment should be added to SOFR or included within a borrower’s specific margin (i.e. for the latter, a two-part loan with only SOFR plus one all-in margin). Failing to separate out the non-idiosyncratic credit spread adjustment could have adverse follow-on consequences for borrowers, particularly non-financial corporates, for whom increased margins are usually indicative of a credit event, such as a ratings downgrade. Providing clarity by referencing a third-party credit spread such as AXI supports the long terms interests of borrowers, but also lenders and policy makers.

5. Avoid unintended consequences

“If everyone is moving forward together, then success takes care of itself.”

― Henry Ford

As we’ve seen, burying the credit spread adjustment within the overall margin on a loan reduces transparency. But it also may unintentionally tighten macro-economic conditions by raising effective overall borrowing rates in the form of “funding insurance.” In times of market stress, credit premiums tend to rise. However, if the credit spread adjustment is embedded within the client margin, it is effectively fixed (rather than a variable credit spread adjustment that floats on top of SOFR). Therefore, banks would have to price the total credit spread at a premium (since it can’t change after that) to compensate them for the risk that funding costs might rise over the life of the loan.

Even then, banks would be exposed to the risk that the “insurance premium” embedded within the margin would not be sufficient to cover large fluctuations in funding costs during a market stress event, such as in March 2020. Likewise, borrowers would be forced to weigh the risk of locking in a higher fixed credit spread adjustment component (which could be a benefit in a market stress event) against accepting a lower dynamic credit adjustment and therefore lower overall interest rate at the inception of the loan. In the latter situation, the borrower is exposed to potentially higher interest rate payments should a market stress event occur.

Policy makers most likely want to avoid pushing borrowers into a position where they have to make bets on interest rate movements (to a greater extent than they already must). Furthermore, from an Official Sector standpoint, the potential for unintentionally higher interest rates, and therefore accelerated tightening of financial conditions in 2022, would not be desirable, especially against the new cloud of uncertainty from the Omicron variant.

6. Be operationally flexible

“It is not the strongest of the species that survives, nor the most intelligent; it is the one most adaptable to change.”

― Charles Darwin

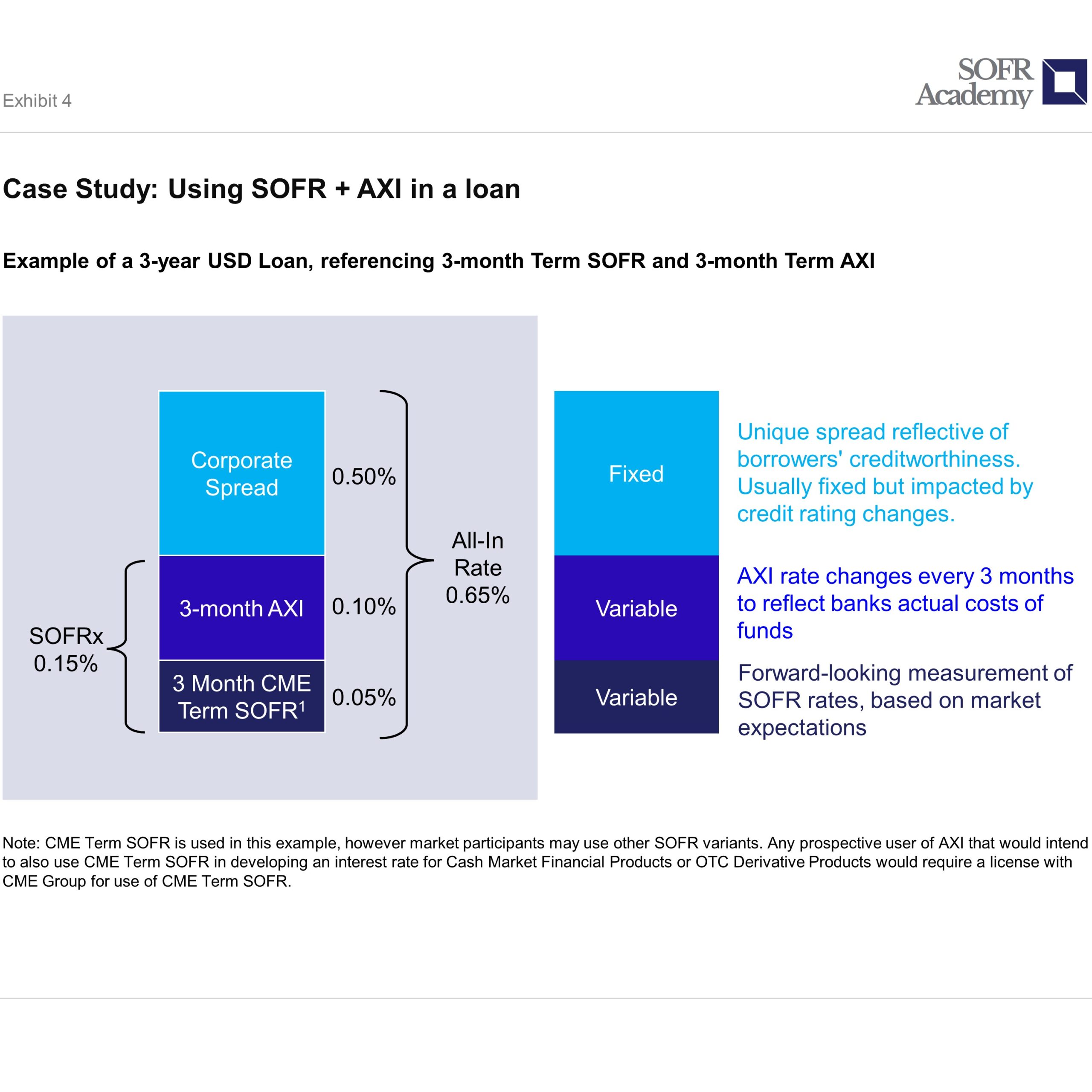

Loan market participants have invested a significant amount of time in recent years ensuring internal systems and process are prepared to handle origination, servicing and trading of non-LIBOR loans. The Loan Syndications & Trading Association’s (LSTA) December 14, 2021 LIBOR Transition Checklist prudently warned that “the SOFR loans that have been executed to date we see that pricing is not structured in a consistent fashion” and that three-part loan pricing (i.e., SOFR + Credit Adjustment Spread (CAS) + Margin) should be understood and supported by internal systems. Major loan system providers have released updates to support risk free rates as well as loan base rates comprised of multiple floating rates. Preparing for the operational flexibility of three-part loan pricing, whether it references AXI or another CAS, allows banks to maximize their lending options while also unifying the financial system in a stable and sustainable way.

SOFR Resources

- SOFR Starter Kit: Includes background, facts and figures about SOFR, and next steps market participants can take.

- SOFR Term Rates Factsheet: A summary of the rationale behind the ARRC’s formal recommendation of forward-looking SOFR Term Rates.

- A User’s Guide to SOFR: An overview of the considerations market participants interested in using SOFR should evaluate.

AXI Resources

- AXI 60-Second Explainer Video: A short YouTube video highlighting AXI’s key features.

- AXI FHFA Supervisory Letter: Provides information on how the FHFA’s supervisory framework can be applied to SOFR + AXI.

- Term SOFR + AXI Concept Credit Agreement: Provides an illustrative example of a credit agreement that references CME Term SOFR + AXI for a syndicated term loan facility denominated in US-Dollars.

- AXI Technical White Paper: Provides detailed information on AXI’s construction methodology

ABOUT THE AUTHOR(S)

Marcus Burnett is Chief Executive of SOFR Academy based in New York. The Firm provides financial education and market data to empower corporations, financial institutions, governments, and individuals to make better decisions. SOFR Academy Inc. is a member of the American Economic Association (AEA), the Loan Syndications and Trading Association (LSTA), the International Swaps and Derivatives Association (ISDA), the Asia Pacific Loan Market Association (APLMA), the Bankers Association for Finance and Trade (BAFT) which is a wholly owned subsidiary of the American Bankers Association (ABA), and the United States Chamber of Commerce.

DISCLAIMER

AXI is not sponsored or endorsed by the Office of the Comptroller of the Currency (OCC) or the Federal Reserve Bank of New York (FRBNY). SOFR Academy is not affiliated with the OCC or the FRBNY nor do they sanction, endorse, or recommend any products or services offered by SOFR Academy.