While the termination of LIBOR, and the subsequent transition to Alternative Reference Rates, present major obstacles today, less attention has been given to the quantitative determinants of these rates. In this article for SOFR Academy, Sven Klingler—Assistant Professor of Finance at BI Norwegian Business School—and Olav Syrstad—economist at the Norges Bank, the central bank of Norway—examine in detail the empirical drivers of Alternative Reference Rates globally. This article is based on their recent research paper, ‘Life after Libor’, which is forthcoming in the Journal of Financial Economics.

In July 2017, the Financial Conduct Authority (FCA) announced that it cannot guarantee the publication of Libor beyond 2021. This announcement, commonly referred to as “Libor funeral”, started a transition toward transaction-based overnight rates, which will serve as alternative reference rates and potentially replace Libor by the end of 2021.

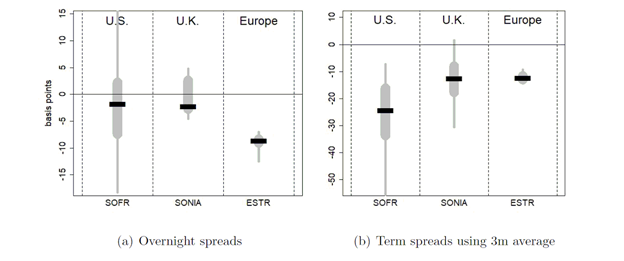

Figure 1 compares the level of the alternative reference rates in the U.S., the U.K., and Eurozone (henceforth Europe) to Libor, or its European counterpart Euribor. Panel (a) shows whisker plots of the spread between the alternative reference rate and overnight Libor in the three regions and Panel (b) repeats the analysis comparing 3-month averages of the alternative reference rates (in arrears) to 3-month Libor.

Panel (a) reveals large fluctuations and inter-country differences—spreads are stable around zero in the U.K., but on average -8.5 basis points in Europe and most volatile in the U.S. with fluctuations between -15 and 15 basis points. The large spreads in Panel (a) are somewhat surprising because we are comparing two overnight rates with low credit risk. Panel (b) demonstrates that the level and volatility of the spreads increases further when comparing 3-month averages of the alternative benchmarks to 3-month Libor.

Figure 1: Spread between the alternative benchmark rates and LIBOR. This figure shows medians (black bars), ranges between the 25% and 75% quantile (thick grey line), and ranges between the 1% and 99% quantiles (thin grey line) for the spread between the alternative benchmark rate in the U.S., the U.K., and Europe relative to LIBOR (for the U.S. and the U.K.) or EURIBOR (for Europe). Panel (a) shows the spread between the alternative benchmark rates and the overnight LIBOR rate (for the U.S. and the U.K.) or the spread relative to EONIA (the overnight EURIBOR rate for Europe). Panel (b) shows the spread between 3-month forward-looking averages of the alternative benchmark rates, computed in arrears, and 3-month LIBOR (for the U.S. and the U.K.) or EURIBOR (for Europe). The sample period starts in August 2014 for the U.S., February 2016 for the U.K., and December 2016 for Europe and include data until December 2019.

Figure 1 raises three questions for the “life after Libor”: (i) Why are the three overnight rates so different? (ii) What drives their dynamics? (iii) How do these differences affect term rates? Answers to these questions have important implications for the transition away from Libor.

To answer the first question, we first note that SOFR is comprised of transactions secured with U.S. Treasuries, while SONIA and ESTR are only underpinned by unsecured transactions. In addition, and more importantly, the underlying transactions can be decomposed into three different types: non-bank lending to banks, bank lending to banks, and bank lending to non-banks. While SOFR is determined by transactions of all three types, both SONIA and ESTR only rely on transactions in which banks borrow from either non-banks or other banks.

Depending on the types of transactions underlying the rate, the lenders’ financial constraints, and the availability of alternative cash placements, overnight rates can be prone to upward or downward spikes. If banks have ample reserves, tighter regulatory constraints lower their demand for borrowing and therefore reduce interest rates. This is the case in the U.K. and Europe, where banks have large amounts of reserves and the alternative reference rates only comprise bank borrowing transactions. By contrast, rates increase with tighter regulatory constraints if banks are in need for cash and reluctant to lend money. This is the case in the U.S., where reserves are concentrated, and the alternative benchmark also reflects bank to non-bank transactions.

Reporting Date Spikes in the Alternative Benchmarks

Table 2 shows that the spread between SOFR and policy target is 20.25 basis points higher at quarter-ends compared to other dates. By contrast, both SONIA and ESTR are lower at quarter-ends, although the size of these differences—on average -2.12 basis points for SONIA and -0.51 basis points for ESTR—is several orders of magnitude smaller.

Table 2: Reporting-date spikes in the alternative benchmark rates. This table shows the results of regressing the alternative benchmark rates on three dummy variables capturing regulatory reporting dates. QEnd equals one on the last trading day of a quarter and zero otherwise, YEnd equals one on the last trading day of a year and zero otherwise, and MEnd\QEnd equals one on the last trading day of a month which is not quarter-end and zero otherwise. Panels (2), (4), and (6) include year-quarter fixed effects. The independent variables are SOFR (Panels (1) and (2)), SONIA (Panels (3) and (4)), and ESTR (Panels (5) and (6)). To remove fluctuations in these rates due to changes in policy rates, we use the spread of these rates over the policy targets in the three regions. The sample periods start in August 2014 for SOFR, February 2016 for SONIA, and December 2016 for ESTR, including data until December 2019. The numbers in parentheses are Newey-West t-statistics. ***, **, and * indicate significance at a 1%, 5%, and 10% level respectively.

Other Drivers of the Alternative Benchmarks

Two other variables affect the alternative reference rates. First, an increase in government debt increases the alternative benchmarks. This increase is due to a “crowding out” effect, where Treasury debt competes with repos for short-term investments. Second, if banks do not have ample reserves, a drop in central bank reserves increases banks’ demand for borrowing and therefore increases interest rates.

As shown in Table 3, we find a strong positive link between the amount of Treasuries outstanding and SOFR. In addition, SOFR increases with transaction volume and a higher amount of bank reserves tends to coincide with drops in SOFR. In the U.K., a higher amount of gilts outstanding significantly increases SONIA and more excess reserves in Europe tend to coincide with lower ESTR. In both the U.K. and Europe, more transactions increase the alternative benchmarks. Contrasting the results for the U.K. and Europe with the U.S. shows that SOFR is more affected by these microstructure effects; especially that fluctuations in the quantity of government debt have a stronger impact on SOFR compared to SONIA and ESTR.

Table 3: Drivers of the alternative benchmark rates in the U.K. and Europe. This table shows the results of regressing changes in the alternative benchmark rates on the indicated variables. Panels (1), (3) and (5) examine daily changes. Panels (2), (4) and (6) examine weekly changes (sampled on Wednesdays). For the U.S., the U.K., and Europe, ∆ log(Debt) are changes in the total amount of U.S. Treasuries, Gilts, or German Treasuries outstanding, respectively. ∆ log(Transact. Volume) are changes in the total trading volume underlying the alternative benchmark rates, and ∆ log(Reserves) are changes in the total amount of bank reserves in the respective area. The independent variables are SOFR (Panels (1) and (2)), SONIA (Panels (3) and (4)), and ESTR (Panels (5) and (6)). To remove fluctuations in these rates due to changes in policy rates, we use the spread of these rates over the policy targets in the three regions. The last, second-last, and first trading day of each month as well as five days after September 15 are removed from the sample to avoid large outliers and reporting-date spikes driving the results. The sample periods start in August 2014 for SOFR, February 2016 for SONIA, and December 2016 for ESTR, including data until December 2019. The numbers in parentheses are heteroskedasticity-robust t-statistics. ***, **, and * indicate significance at a 1%, 5%, and 10% level respectively.

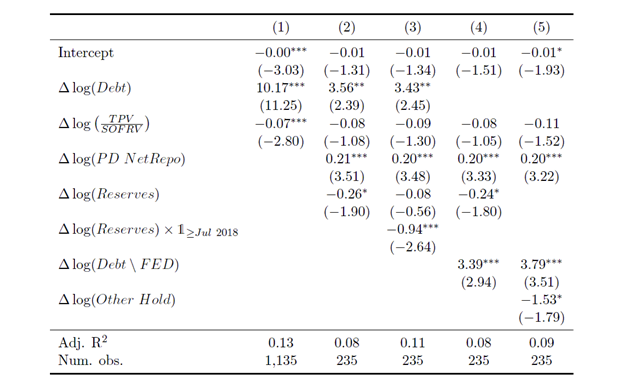

Motivated by these findings and by our hypotheses, we next examine changes in SOFR more closely (Table 4). We construct a proxy of the fraction of non-bank to bank lending in SOFR and find that this proxy together with the amount of government debt outstanding explains 13% of the daily variation in SOFR on non-reporting dates. In addition, more demand for repos from primary dealers increases SOFR. Finally, the impact of changes in reserves on SOFR strengthens between mid-2018 and late 2019, when reserves in the U.S. became less abundant.

Table 4: What makes SOFR tick? This table shows the results of regressing changes in SOFR on the indicated variables. To avoid capturing fluctuations in SOFR due to changes in the policy target rate, we analyze the spread between SOFR and the upper bound of the of the Federal Fund’s target rate. ∆ log(Debt) are changes in the total amount of Treasuries outstanding, ∆ log(TPV/SORFV ) are changes in the fraction of triparty repo in SOFR, ∆ log(PD NetRepo) are changes in the net amount of overnight repos of primary dealers, ∆ log(Reserves) are changes in the total amount of bank reserves in the U.S., 1≥Jul 2018 is a dummy variable that equals from July 2018 on and zero otherwise, ∆ log(Debt FED) are changes in the amount of Treasuries outstanding minus FED Treasury holdings, and ∆ log(Other Hold) are changes in the amount of non-Treasury securities on the FED balance sheet. Panel (1) examines daily changes, Panels (2)–(5) examine weekly changes (sampled on Wednesdays). The last, second-last and first trading day of each month as well as five days after September 15 are removed from the sample to avoid reporting-date spikes or the large September 15, 2019 spike driving the results. The sample period is August 2014 to December 2019. The numbers in parentheses are Newey-West t-statistics. ***, **, and * indicate significance at a 1%, 5%, and 10% level respectively.

The Impact on Term Rates

While microstructure effects have a first-order impact on overnight rates, a large part of the spread between average overnight rate and 3-month Libor, illustrated in Figure 1, Panel (b) is driven by the term premium in Libor. The term premium includes a liquidity premium to compensate lenders for committing funds over longer time-periods and a credit premium to compensate lenders for the risk of default. By contrast, term rates based on the alternative reference rates will be averages of overnight rates and therefore lacking a term premium. We use averaging in arrears and decompose the spread between alternative benchmarks and 3-month Libor into two components—a proxy for the term premium in Libor and the spread between the alternative reference rate and overnight Libor.

Figure 5 shows the results of this decomposition. As we can see from the figure, the term premium occasionally exceeds -50 basis points in the U.S., reaches almost -40 basis points in the U.K., and is between 0 and -5 basis points in Europe. In addition, Figure 5 shows that the U.S. SOFR-Libor overnight spread exhibits large variation between -20 and 15 basis points, with a noticeable spike in mid-2019 while the same spread in the U.K. is stable with the only noticeable change in 2018, when the Libor reform lead to a decrease in Libor. In Europe, the term spread is virtually constant at 8.5 basis points and significantly larger than the term premium.

Figure 5: Spread between 3-month average of alternative benchmarks and Libor. This figure decomposes the spread between 3-month averages of the alternative benchmarks, computed in arrears, and 3- month LIBOR into a term spread component and benchmark spread component. The light-shaded areas show the component of the spread due to term premium. This component is estimated as the spread between the 3-month average of overnight LIBOR (or EONIA; both computed in arrears) and 3-month term LIBOR. The dark-shaded areas show the component of the spread due to differences in overnight rates. This component is computed as the 3-month average of the spread between the alternative benchmarks and overnight LIBOR. On days where the spread between overnight rates is positive, the term premium is the sum of the light- shaded and dark-shaded areas in the graph. On days where the term premium component is positive, the term premium is the sum of the light-shaded and dark-shaded areas in the graph.

Conclusion

While the transition away from Libor to alternative reference rates will enhance the transparency and robustness of benchmark rates, our paper highlights three potential challenges for the “life after Libor”. First, the composition of transactions underlying the alternative benchmarks affect the interest rates and introduce volatility unrelated to banks’ marginal funding costs. This effect is the strongest for SOFR. Second, we show that the supply of government debt affects the alternative reference rates. For the secured rate SOFR, the impact of government debt supply is even more pronounced because the rates are also affected by the availability of government debt collateral. Third, we decompose the spread between each overnight alternative reference rate and the corresponding term Libor into an overnight credit spread and a term premium. The magnitude and volatility of the two components vary substantially across jurisdictions.

Sven Klingler is Assistant Professor of Finance at BI Norwegian Business School and Olav Syrstad is an economist at the Norges Bank, the central bank of Norway. Their full research paper can be found here. This note should not be reported as representing the views of Norges Bank. The views expressed are those of the authors and do not necessarily reflect those of Norges Bank.