The fact that the so-called risk-free rate (RFR) benchmarks – SOFR most prominent among them – refer to overnight rates rather than term rates makes these benchmarks fundamentally different from the interbank offer rates (IBORs) they are meant to replace. This difference goes beyond credit spreads, which reflect that the borrowing transactions informing SOFR are secured, while IBOR borrowing is unsecured.

In this article for SOFR Academy, Professor Erik Schlögl – Director of the Quantitative Finance Research Centre at the University of Technology Sydney – explains how the tenor basis in interest rate markets reveal a market premium for refinancing risk faced by short-term borrowers, and how this confounds attempts to obtain term rates from overnight rate benchmarks by way of derivative instruments, say overnight index swaps (OIS), or averaging (SOFR Averages or SOFR Index). This article is based on a recent research paper by Alex Backwell, Andrea Macrina, David Skovmand and Erik Schlögl.

First, some background on the points more commonly raised in the SOFR debate: Replacing IBORs with transaction–based RFRs lives up to the objective of moving toward a primary benchmark that is both closely related to actual transactions and less susceptible to manipulation. However, the transition to RFR benchmarks such as SOFR raises the question whether SOFR is an appropriate proxy for actual interbank (or, for that matter, corporate) funding cost, as well as the issue of converting existing contracts referencing IBORs to SOFR equivalents. While the latter problem is of considerable magnitude, the resolution of the former is a pre–requisite for satisfactorily addressing this – something which is only beginning to be discussed in earnest:

- In response to a letter from a group of bank representatives, the Board of Governors of the Federal Reserve System, the US Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation established a LIBOR Transition Credit Sensitivity Group (CSG), “to focus on the issues surrounding a credit sensitive rate/spread that could be added to SOFR”. Here, the issue raised by the group of bank representatives, and thus the issue which the CSG seeks to resolve, is one of a disconnect due to credit risk between the cost of funding of private–sector banks (subject to credit risk) and a SOFR benchmark based on repo transactions (subject to negligible credit risk). The mismatch in tenor between the new candidate benchmarks (i.e., overnight) and the old IBOR benchmarks (e.g., three months, six months, etc.) is not addressed.

- In the broader debate, problems arising from this mismatch typically are only mentioned in passing. This may be because of the hope that “term rates” based on SOFR will become available once SOFR is well–established as the market benchmark, based on OIS referencing SOFR as the overnight rate (in a manner similar to how current OIS contracts reference the overnight Effective Fed Funds Rate). Alternatively, a consultation by the ISDA suggested that a backward–looking approach, where a (constant) term– and currency–dependent spread is added to a compounded average of SOFR, is the preferred option for replacing LIBOR in existing derivatives.

In a recently updated paper, Alex Backwell, Andrea Macrina, David Skovmand and I conclude that neither of these approaches leads to benchmarks with the term–rate properties of the old IBOR benchmarks. In particular, SOFR–based term rates implied from OIS contracts would be more suitable to replace the current OIS–implied term rates based on Fed funds, not the benchmark IBORs. Intuitively, this is both unsurprising (though largely unrecognised) and economically significant when one considers that tenor basis spreads (between one–month, three–month and six–month tenors, and between these tenors and OIS) are known to be substantial and volatile. From a perspective of sound mathematical modelling and the associated econometric analysis – documented in the paper – this is due to “roll–over risk.” This is the risk a borrower faces when they refinance their debt at a future time and the spread to the market benchmark rate, at which they are able to roll over debt, increases. In general, this consists of downgrade risk (an aspect of credit risk quite distinct from that considered by the CSG) and funding liquidity risk – though for secured borrowing one would only consider the latter.

“In particular, SOFR–based term rates implied from OIS contracts would be more suitable to replace the current OIS–implied term rates based on Fed funds, not the benchmark IBORs.”Professor Erik Schlögl – Director of the Quantitative Finance Research Centre at the University of Technology Sydney

Pricing roll–over risk

The basic argument that the market puts a price on roll-over risk goes as follows:

- In the market, we observe tenor basis spreads between rates of different roll-over frequencies, for example in a basis swap exchanging a three-month floating rate for a six-month floating rate, but also in the IBOR/OIS spread, where the rate underlying the floating leg of an OIS has a daily roll-over frequency.

- Naively, these spreads would suggest an arbitrage opportunity – to take advantage of this, one would lend at the longer tenor and borrow at the shorter tenor. If interest rate risk were the only risk (e.g., the fluctuations of IBOR), this strategy combined with the appropriate basis swap would indeed be riskless, and would earn the basis spread as an arbitrage profit.

- The fact that basis spreads persist in the market means that there must be other risk, blocking this arbitrage channel. In our view, the main risk in the above strategy is that the arbitrageur may not be able to roll over the (shorter tenor) debt at the benchmark rate (e.g. IBOR) in the future, but will have to pay a higher rate. This is “roll-over risk”.

Thus, basis spreads (and the IBOR/OIS spread) represent a premium which longer-term borrowers pay to avoid roll-over risk. In this sense, there is an equivalence between basis spreads and the more classical concept of a term premium.

Model estimation

As noted above, one component of roll-over risk is credit risk (or, more accurately, credit spread risk) – if the arbitrageur suffers a downgrade, their borrowing rate goes up relative to the benchmark. The other component we call (for the lack of a better word) “funding liquidity risk” – one way one can interpret this is the fear of a repeat of what happened around the time of the Lehman Brothers default, where IBOR was quoted, but it was difficult or impossible to borrow. It is not a coincidence that basis spreads greatly increased during that time. Though these spreads have dropped since then, they are still above their pre-crisis levels – one could say that during that crisis the market “learned” to price roll-over risk.

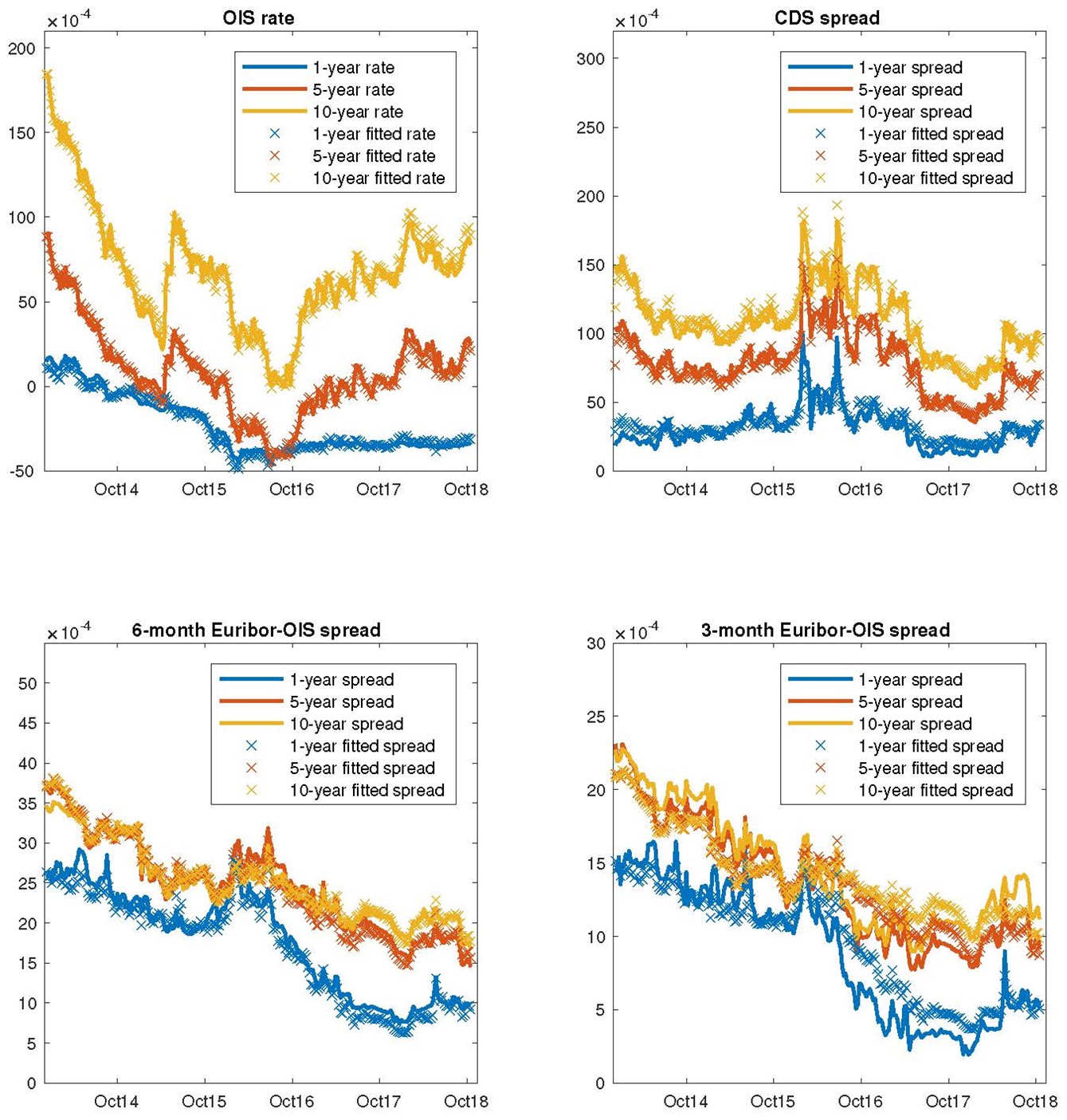

Our model estimation to date focuses on euro data, but one would expect qualitatively similar results in all currencies in which there are basis spreads. Since our model combines interest rate, credit and funding liquidity risk, it is estimated on a dataset comprising OIS rates for maturities from one to ten years (7 maturities), vanilla interest rate swaps (7 maturities), credit default swaps (8 maturities) for EURIBOR panel member banks, and basis swaps (7 maturities) swapping three-month for six-month EURIBOR. Estimating a constant parameter model on time series data from 2 January 2014 to 24 October 2018 using the unscented Kalman filter, we obtain a very good fit to market data, especially considering the large number of instrument maturities. This is illustrated in Figure 1.

If downgrade risk were the only risk driving basis spreads, roll-over risk would be moot to the debate around the transition to the new RFR benchmarks, where credit risk is mitigated through repo transactions. The econometric results reported in our paper, however, show that this is not the case. We find that credit risk typically contributes only about 30% of the IBOR/OIS spread. The balance of the IBOR/OIS spread is due to the funding liquidity component of roll–over risk, which we have modelled more explicitly than the prior literature. Figure 2 illustrates this on the EURIBOR/OIS spread, showing the fitted spread (with the six– and three–month tenor in either panel) as well as the spread our model implies based solely on credit risk.

Downgrade risk and roll–over risk

We note that downgrade risk never explains a dominant part of the observed spreads. It tends to constitute a significant part of the total roll–over risk, but well less than half, and the contribution is small for short–term spreads when spreads are low (in late 2017 and early 2018). This leads us to also consider a specific instance of our framework in which credit risk (and with it, downgrade risk) is “turned off,” leaving only the funding–liquidity component of roll–over risk. That is, our framework is equally applicable in an interest rate market in which credit risk is completely mitigated by collateralisation. This highlights how the presence of roll–over risk confounds efforts to create proper term rate benchmarks based solely on contracts referencing SOFR:

- If one replaces the (unsecured) overnight Fed funds rate underlying an OIS by SOFR, then a family of such OIS for a set of maturities will imply a term structure of rates and discount factors. However, even in the absence of any market imperfections, these rates will differ from rates for secured borrowing at term (i.e., repo term rates), due to roll–over risk (now based solely on funding-liquidity, not credit, risk). That is, we would expect an OIS/repo term rate tenor basis.

- Neither will this problem be resolved by averaging SOFR over some longer accrual period, nor by compounding the SOFR on a unit of investment over time, which are additional benchmarks published by the Federal Reserve Bank of New York under the names SOFR Average and SOFR Index. Aside from not being proper term rates, these rates are not known until the end of the accrual period, rather than at the beginning. While the technical issues involved in pricing contracts which reference backward–looking rates are surmountable, irrespective of roll–over risk, the backward–looking averaging means that SOFR Average and SOFR Index will have a much lower volatility than fixed–in–advance spot term rates, be they unsecured (LIBOR) or secured (repo term rates). This issue is removed when one considers the forward rates implied by futures on SOFR Averages, at least as long as the beginning of the averaging period still lies in the future. However, even after the appropriate convexity adjustments, we would still expect a tenor basis between such forward rates and the corresponding repo forward term rates due to roll–over risk.

Conclusion

Thus, we have seen why proper term rates based on the new RFR benchmarks remain elusive: By definition, benchmarks based on overnight rates cannot reflect a term premium, which we have made more explicit as the premium that borrowers are willing to pay in order to avoid the risk associated with having to roll over short-term debt. Having extracted this premium from the tenor basis prevalent in interest markets and decomposed it into a credit and a funding liquidity component, we see that basis spreads and term premia will persist when credit risk is mitigated. This leads to a fundamental distinction between SOFR (including indices, averages and derivative instruments referencing SOFR) and term rates at which market participants actually can borrow.

Professor Erik Schlögl is Director of the Quantitative Finance Research Centre at the University of Technology Sydney, Alex Backwell is a Senior Lecturer at the African Institute of Financial Markets and Risk Management at the University of Cape Town, Andrea Macrina is a Reader in Mathematics at University College London and David Skovmand is an Associate Professor in Financial Mathematics at the University of Copenhagen. Their full research paper can be found here.